My lessons from 4 years in venture capital

This week, I turned 24. That roughly marks 8 years since I started trying to make a dent in the world with technology and 4 years since I started trying to make a dent with capital. It’s also a good opportunity to reflect. For the sake of whatever this is, I’m collecting my thoughts on the state of technology and capital, not everything I’ve learned and gained personally. That is for a different time, a different place, and, potentially, a different set of eyes. Lastly, NONE of this is financial advice.

There are no bubbles in tech

It’s fancy to call everything a bubble now. To me, a bubble is an artificial inflation in asset prices that leads to permanent capital loss during its crash. The Dutch Tulip Mania is a great example: a single tulip wasn’t, isn’t, and is likely never going to be worth 3 years of an average Dutchmen’s pay. The bubble was fake and it popped.

That just isn’t true in tech. It may be fair to say that at any given point in time, technology assets are over valued. But, unlike other bubbles that create permanent capital losses, advances in technology create so much value that any capital losses can often be recovered and turn into large profits in the long run.

A great example of this: Invesco launched the QQQ in 1999 as an Innovation ETF focused on tech stocks. That was the height of the so-called “Dot Com Bubble”. In its first couple years, it lost 80% of its value. Easy to call that a bubble and mock anyone who invested. 26 years later, the QQQ has returned 1177.30%, or roughly 13 times, while the S&P 500, which only saw its value cut in half during the Dot Com Bubble, is up just 682.35%, or nearly 8 times.

Market sizing makes you poor

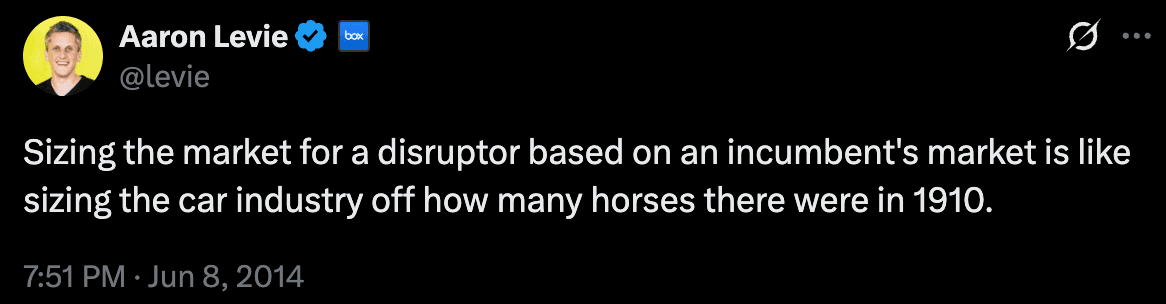

Venture investors, like every other public or private equity investor, love to rhapsodize about the importance of TAM and market sizing. As someone who has been a junior investor at multiple funds, I, too, have had the privilege of trying to make up numbers to defend our decision to IC.

However, more often than not, market sizing is used as a cudgel on why not to do a deal. “The TAM isn’t big enough.” “This will never be a $10B company.” Blah, blah, blah.

The problem is no one fucking knows. I love this quote from my fellow Trojan alum, Aaron Levie:

Stop wasting your time on public comps and missing out on true disruptors! As a venture investor, your job is to find batshit crazy founders who are solving a truly difficult problem. The score, as Bill Walsh says, takes care of itself.

Ambition’s tragedy of commons

There are myriad critiques of what happens when money is free flowing and the cost of capital is low. Companies raise too much, they burn too much, they blow up. I’m just as concerned about a different symptom I’m seeing: when founders can quit their job and raise $5M the next day, being a founder attracts a certain kind of less risk-on person.

I’m not saying the accessibility of money is a bad thing; it isn’t. But, the thinning of founders who believe they were given a Divine Mandate and need to conquer the world like Napoleon or Caesar is profoundly disappointing. The DPI equation on founders selling for $50M is rough, the societal impact of them giving up is even worse.

Real capitalists burn money

Every venture investor loves to “push for austerity” or tell their portfolio companies to be “default alive”. After all, it sounds difficult and thus must be rewarding in some way, right? How cute.

It’s actually quite easy for a revenue generating software business to not burn money. Especially with the rapid rate of revenue growth in AI land.

I want to invest in founders who have allocation discipline not “spending discipline”. Your job as a CEO is to be thoughtful about where to deploy capital, not debating whether you deploy it at all. I don’t want my founders to optimize for free cashflow. No software company needs a fortress balance sheet.

In fact, to me, that’s a negative indicator; it’s an indication that they no longer know where to invest capital. Or even worse, they know where to put capital but are too afraid to do it.

If you’re trying to make a billion dollars, you won’t get there picking up pennies.

Traditional finance is unserious when it comes to tech

I graduated from USC with an undergraduate degree in Business Administration. I realized, at the time, that half of my classes were deeply unserious. When my “Leadership” professor bragged to us that his original syllabus was so good that he hadn’t changed it in 20 years, I realized that everything in the textbooks (that I refused to buy or read) was probably bullshit. I did think, however, at the time that some of our quantitative classes like “Business Finance” were materially helpful.

Unfortunately, hindsight tells me I was wrong about that too. Some reasons were obvious and recognizable at the time; obviously the Efficient Market Hypothesis makes zero sense in practice. But I never realized how broken traditional finance is when it comes to technology.

I laugh every time one of my investment banker friends tells me about his or her model that includes some terminal growth assumptions. If an analyst told their MD, between tears at 4am, that Microsoft would be growing at 15%+ 39 years after its IPO, they would’ve been told to go home and look for a new job. After all, “no company can outgrow the US GDP in the long run”. Turns out the long run can just be really fucking long.

P.S. I would LOVE to see the reactions of erudite public markets investors to any banker who tried putting half a trillion dollars of Remaining Performance Obligations in any Oracle capital markets deck over the last twenty years.

Ruling out the counterfactual

One thing that many venture investors borrow from traditional finance is the framework of thinking about what it would take to make something work. This works quite well in private equity for example. You can map, fairly linearly, the set of events that would need to occur to get a 3x MOIC in 5 years. In venture, that works when you're investing in market risk. ACV x penetration rate x TAM.

However, the real money in venture is made investing in technical risk. The moonshot bets that enable a new world. Not B2B SaaS incrementalism. If you could map technical risk linearly, it probably isn't really technical risk. And for that, our job is not to map out why the business COULD work, it's to ensure there are no reasons why it obviously WON'T work.

This applies to all technology risk capital allocation. A good example is Waymo. Sebastian Thrun recounted that when he told Larry Page that self-driving cars wouldn't work, Larry asked him: "Ok, you say it can't be done. You're the expert. I trust you. So I can explain to Sergey why it can't be done, can you just give me a technical reason, why it can't be done?" Sebastian didn't have a concrete answer so they embarked on a mission to test it. Larry recognized that you didn't need to know how Waymo certainly would work; you just needed to know that there was no reason it certainly wouldn't. Over 10 million paid rides later, it's clear it pays to bet on "uncertain".

The future will be better

Lastly and most importantly, 8 years watching technology has taught me that it is always better to bet on the future than the past.

When I founded Chromata 8 years ago, there was a certain urgency with which the people around me moved, not because they needed to get somewhere, but because they felt like the world was changing around them and it would be too detrimental to let it pass by. That commotion is exciting; it gives me hope that these people (and I hope to be one of them) will continue to push the arrow of humanity forward. It’s also convinced me that as a capital allocator, you should be levered long the future. As Nat Friedman said: “Pessimists sound smart. Optimists make money.”

I’ll close with a quote from Atlas Shrugged that I believe captures the spirit of venture capital and startups incredibly well:

“Do not let your fire go out, spark by irreplaceable spark, in the hopeless swamps of the approximate, the not-quite, the not-yet, the not-at-all. Do not let the hero in your soul perish, in lonely frustration for the life you deserved, but have never been able to reach. Check your road and the nature of your battle. The world you desired can be won, it exists, it is real, it is possible, it’s yours."